Too often, individuals who have been severely-injured in big rig crashes are forced to sue to get repayment of even the most basic of medical care. Truck carriers just push the lawsuit on to their insurance companies. Every trucking company, big or small, must carry insurance coverage, with some carriers having millions of dollars in BIPD (“Bodily Injury & Property Damage”) insurance, as well as bond and cargo insurance. But those big profit-center carriers are the exception: far too many companies (even those generating millions and millions of dollars in revenue a year) are woefully underinsured.

How much insurance do trucking companies have?

Commercial truck insurance minimum requirements have been the same for over four decades. For an American general freight trucking carrier, $750,000 in general liability insurance is the minimum insurance amount. (This figure is higher for trucks carrying hazardous freight, but that figure has also remained the same since 1982.) If the liability limits were adequate when the legislation was enacted, then the current equivalents would be two to four times the original levels. Simply adjusted for inflation, this insurance minimum should be increased to nearly $3 million today. Yet, the antiquated, 40-year-old insurance requirement remains the same dollar amount required today.

And how much does this cost the multi-million dollar trucking company? Just a couple hundred dollars a month in premiums per year. In theory, this insurance covers all damages for every truck driver in a fleet. In reality, this is simply not enough to make a dent in a severe truck crash case.

A history of insurance minimums

In an effort to remove the barriers to entry and encourage competition and innovation, Congress deregulated the trucking industry in 1980. Yet, there was a concern that a flood of inexperienced and undercapitalized carriers would enter the market and fail to maintain adequate safety standards or lack sufficient financial resources to compensate for damages caused. So Congress set the minimum insurance levels for property transport to $750,000 and hazardous materials insurance to $5 million.

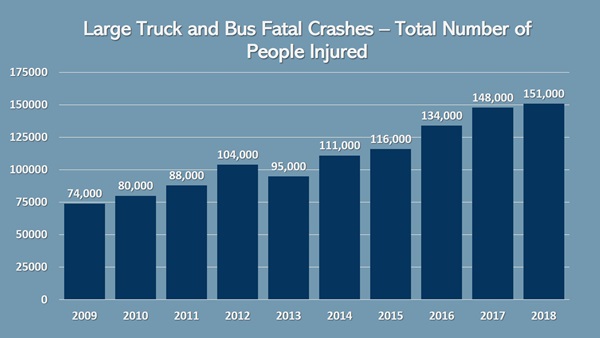

The trucking carrier insurance guidelines (1980) were written at a time when just 27,000 carriers were in operation. Today, there are almost a million for-hire carriers as well as over 800,000 private carriers in business. Yet, insurance minimums have remained unchanged since 1980, not even remotely keeping pace with the rate of inflation or the changing dynamics of truck accidents today. According to the FMCSA, truck crashes and fatalities have more than doubled in just the past 10 years… and that doubling effect goes back even further.

Source: American Association of Justice, “Raise Trucking Insurance Minimums to Raise Safety”

When minimum insurance coverage is not enough

“There is considerable anecdotal evidence of instances of full compensation denied because of insufficient insurance or legal obstacles.” – FMCSA, 2013

What happens when a trucking company is responsible for an accident with damages that far exceed their insurance coverage? The insurance company will quickly try to settle, “interpleading” the carrier’s low insurance limits. This essentially means putting the limited amount of money in one pot, pitting injured parties against each other to fight over a meager payout.

What if the trucking company loses at trial, forced to pay a verdict in excess of their insurance policies? Many will simply go out of business and start a new venture under a different name. “Chameleon carriers” demonstrate the general lack of scruples and oversight within the industry as a whole. Such was the case with Castellano 03 Trucking; according to local news sources, this truck carrier dissolved shortly after one of their drivers caused the fatal 28 car pile-up, killing four people on I-70 in Colorado. Just one day after the crash, a second company operating from the same home address, Volt Trucking LLC, applied for a new business license. This is how easy it has become for trucking companies to shirk responsibility. (To note: larger trucking companies rarely use this tactic, as they tend to have larger insurance policies in the $20-$50 million range or more.)

How much insurance coverage is enough?

According to the Department of Transportation, the average truck accident resulting in fatality can be higher than $7.2 million. The price tag goes up from there depending on the extent of damage, cause of accident and the types of injuries. For example, if a permanent disability or lifetime physical impairment occurred, that number would go higher due to the long-term care or treatment necessary.

With that in mind, both the Truck Safety Coalition and The Pacific Institute for Research and Evaluation (PIRE) recommend that property-transporting truck companies should carry a minimum of $10 million.

But, some wonder, can trucking companies afford these premiums? In short: yes. At present, insurance makes up only about 4% of truck carriers’ costs, or just seven cents per mile. Meanwhile the trucking industry made $792 billion in revenue in 2019.

The benefits of raising insurance minimums

• Reduce the exporting of crash costs onto the general public. If the minimum levels of coverage increase, the injured person would be able to afford medical care, future medical care, etc. with the help of the truck carrier’s insurance monies. If not, the injured person may need to rely on taxpayer funded government assistance or Medicaid to get the necessary medical treatment.

• Remove unsafe carriers from the industry. If high-risk behavior such as unsafe driving and poor maintenance are associated with financially unhealthy carriers, increasing the minimum insurance levels may remove marginally profitable unsafe carriers from the roads.

• Reduce risk for smaller carriers. Increased insurance minimums would also help smaller, owner-operator truck carriers. For a few cents on the dollar, “mom-and-pop” companies would be required to get better insurance coverage, ensuring that any severe crash would be paid out by the insurer – and not affect the small business owner.

A simple answer

The Federal truck insurance minimums are an outdated relic from an era of deregulation and lower highway risks. Adjusting for inflation takes the $750,000 minimum up to nearly $3 million today; the added premium costs are nominal for a revenue-generating trucking company. Increasing truck carriers’ insurance minimums is a smart move for the trucking industry and for everyone who shares the road.